Good day everyone, at

the last lecture we have completed the second chapter: Identifying Competitive

Advantages. In this chapter we were explained why competitive advantages are

typically temporary, described each five of the forces in Porter’s Five Forces

Model, comparing all the generic strategies and described the relationship

between business processes and value chain.

In order for a leader to run a company these days, the leader must

ensure that all of his employee are heading in the right direction and

completing their goals and objectives.

Identifying Competitive Advantages.

From what I understand,

competitive advantages are a piece of product or service that customer place a

greater value than they do on similar offerings from competitor. Competitive

advantages provide the same product or service either at a lower price or with

added value that can fetch the best price. However, competitive advantages are

typically temporary as competitors often seek ways to compete. Another

advantage is First mover advantages which means when an organization can

significantly influence its market share by being first to market with a

competitive advantage. For example, FedEx created a first mover advantage by

developing its customer self-service software that allows people to request

parcel pickups and track parcels online. Other company quickly began building

their own online company. Also, organizations watch their competition through

Environmental scanning which means the acquirement and analysis of events and

trends in the environment external to an organization.

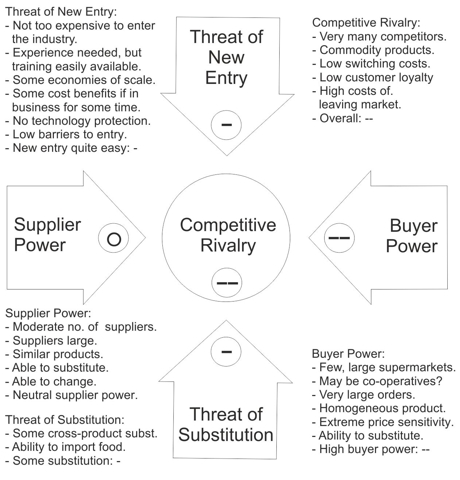

The Five Forces Model

In this model, it

formally analyses the competitive forces within the environment in which a

company operates to assess the possibility for profitability.

The Three Generic Strategies

Organization follows

this strategic when entering a new market.

o Broad market and low cost – The business strategy is

to be low cost provider of goods for the cost conscious consumer.

o Broad market and high cost – its business strategy

offers a variety of specialty and upscale products to affluent consumers.

o Narrow market and low cost – Offer specific product

at low prices.

o Narrow market and high cost – its business strategy

allows it to be a high cost provider of premier product to affluent consumer.

Value Creation

Lastly, once an

organization chooses its strategy, it can use tools such as the value chain to

determine the success or failure of its chosen strategy.

Thank you for reading! Hope you enjoyed it and understood

what I wrote. Till next chapter.

No comments:

Post a Comment